#FactCheck: Viral Video Showing Pakistan Shot Down Indian Air Force' MiG-29 Fighter Jet

Executive Summary

Recent claims circulating on social media allege that an Indian Air Force MiG-29 fighter jet was shot down by Pakistani forces during "Operation Sindoor." These reports suggest the incident involved a jet crash attributed to hostile action. However, these assertions have been officially refuted. No credible evidence supports the existence of such an operation or the downing of an Indian aircraft as described. The Indian Air Force has not confirmed any such event, and the claim appears to be misinformation.

Claim

A social media rumor has been circulating, suggesting that an Indian Air Force MiG-29 fighter jet was shot down by Pakistani Air forces during "Operation Sindoor." The claim is accompanied by images purported to show the wreckage of the aircraft.

Fact Check

The social media posts have falsely claimed that a Pakistani Air Force shot down an Indian Air Force MiG-29 during "Operation Sindoor." This claim has been confirmed to be untrue. The image being circulated is not related to any recent IAF operations and has been previously used in unrelated contexts. The content being shared is misleading and does not reflect any verified incident involving the Indian Air Force.

After conducting research by extracting key frames from the video and performing reverse image searches, we successfully traced the original post, which was first published in 2024, and can be seen in a news article from The Hindu and Times of India.

A MiG-29 fighter jet of the Indian Air Force (IAF), engaged in a routine training mission, crashed near Barmer, Rajasthan, on Monday evening (September 2, 2024). Fortunately, the pilot safely ejected and escaped unscathed, hence the claim is false and an act to spread misinformation.

Conclusion

The claims regarding the downing of an Indian Air Force MiG-29 during "Operation Sindoor" are unfounded and lack any credible verification. The image being circulated is outdated and unrelated to current IAF operations. There has been no official confirmation of such an incident, and the narrative appears to be misleading. Peoples are advised to rely on verified sources for accurate information regarding defence matters.

- Claim: Pakistan Shot down an Indian Fighter Jet, MIG-29

- Claimed On: Social Media

- Fact Check: False and Misleading

Related Blogs

.webp)

Executive Summary:

On July 4, 2024, a giant password dump, “RockYou2024” was posted on a cybercrime marketplace containing 9,948,575,739 plain-text credentials. This blog explains the technical aspects of this leakage and its consequences in the sphere of information security.

RockYou2024 is a list of passwords obtained from different data breaches ranging over the course of more than twenty years. It integrates older passwords with the lexical database with the additional passwords from the recent hacks, thereby, cumulating the database of genuine and existing passwords. The compilation is said to contain data from more than 4,000 databases putting the tool in the hands of potential attackers. RockYou owns the name to this type of attack since a data breach attacked a social media company named , “RockYou'' and released 3.2 million users’ passwords as a .txt file. Since then, the term gained a common meaning connected with mass password data breaches.

Technical Implications:

- Credential Stuffing Attacks: The RockYou2024 list comprises a great number of actual passwords that increases the likelihood of credential stuffing attacks. With this, the attackers help themselves with an opportunity to try to gain unlawful access into several online accounts that a user may have, particularly ones where an individual re-uses the same password.

- Brute-Force Attacks: The collection is extensive for brute force attack on systems that have no protection against such exercise. This is especially the case for devices and services that are exposed to the internet and which may use either weak or factory-set alphanumeric codes.

- Password Cracking: Web compilations that include such lists are often employed by security specialists and penetration testers who use John the Ripper or Hashcat to check the password’s strength or the system’s susceptibility to attacks.

- Machine Learning Models: The dataset could be used to create machine learning models for password prediction or analysis, which would only lead to further better methods to be used in the attacks.

Countermeasures / Mitigation:

Below are the technical risk/process operating proposed to reduce the risks associated with RockYou2024:

- Password Hashing: It is necessary to ensure that all the passwords required to be saved should be encrypted in one of the most secure algorithms like bcrypt, Argon2, or PBKDF2 along with a reasonable number of iterations.

- Salt and Pepper: The features for both salting and peppering should also be enabled to complicate the cracking of passwords even after the hashed password databases have been procured.

- Multi-Factor Authentication (MFA): Ensure the usage of complex passwords in addition to deploying MFA across all the technological systems and services within the company.

- Password Strength Policies: Adhere to password policies for features like the length, strength of the passwords and the change in password frequency.

- Rate Limiting and Account Lockouts: Inactivity methods must be used on consecutive attempts to log in and to the temporary lock out after so many attempts in a bid to discourage brute force attacks.

- Monitoring and Alerting: There should be measures in place to monitor for any violations such as login tappings or a form of credential stuffings and there should be alerts, where securities risks are likely to arise, in real time.

- API Security: The following proper API security measures that will result in the prevention of the following attacks; rate limiting, input validation, and token.

- Web Application Firewalls (WAF): To defend against threats from the internet for potential credential stuffing or brute-forcing the authentication process, utilize WAFs to operate at the application layer.

Analyzing the Impact:

To understand the potential impact of RockYou2024, organizations should assess the possible effects of RockYou2024, such as:

- Conduct Password Audits: LeakYou2024 scan current passwords database with RockYou2024 (in ethical and safe methods) and see which accounts have been compromised.

- Implement Continuous Monitoring: If this is a monthly or weekly event then there must be new information on data breaches and act on it concerning new security changes.

- Educate Users: Continued security consciousness training, regarding the effective protection of an individual’s password in combination with a password generator.

- Perform Penetration Testing: It is suggested to conduct penetration testing at least twice a year to find out if there are vulnerabilities in the systems and applications in the current use.

Conclusion:

The RockYou2024 leaked password database is a serious security risk; it contains almost 10 billion account credentials. This unprecedented leak further increases the exposure to credential stuffing, brute force and password cracking attacks. To deal with these threats, organizations need to have measures that include password hashing, multi-factor authentication, password strengthening and password audit. Patching, user awareness, bandit activities are imperative to prevent future invasions and strengthen the cyber security posture.

References :

- https://statanalytica.com/blog/rockyou-2024-txt-password/

- https://dig.watch/updates/rockyou2024-password-leak-exposes-nearly-10-billion-unique-passwords

- https://complexdiscovery.com/rockyou2024-leak-nearly-10-billion-passwords-exposed-heightening-cybersecurity-risks-for-businesses/

Executive Summary

A postcard featuring BJP leader Manoj Tiwari is being widely shared on social media with a purported statement attributed to him. The viral postcard claims that Tiwari suggested that if people stopped using the ₹1 coin and treated ₹2 as ₹1, the value of the dollar would automatically come down to ₹45. Users are sharing the post claiming that the BJP leader made the bizarre suggestion to strengthen the Indian rupee against the US dollar.

However, research by the CyberPeace Research Wing found the claim to be false. Manoj Tiwari never made any such statement regarding the rupee and the dollar. The BJP MP himself has dismissed the viral claim as fake.

Claim

TMC leader Kirti Azad shared the viral postcard on X and wrote, “As received on X, forwarded as it is. India is truly blessed with such brilliant minds.”

https://x.com/KirtiAzaad/status/2055905987115233473?s=20

Fact Check

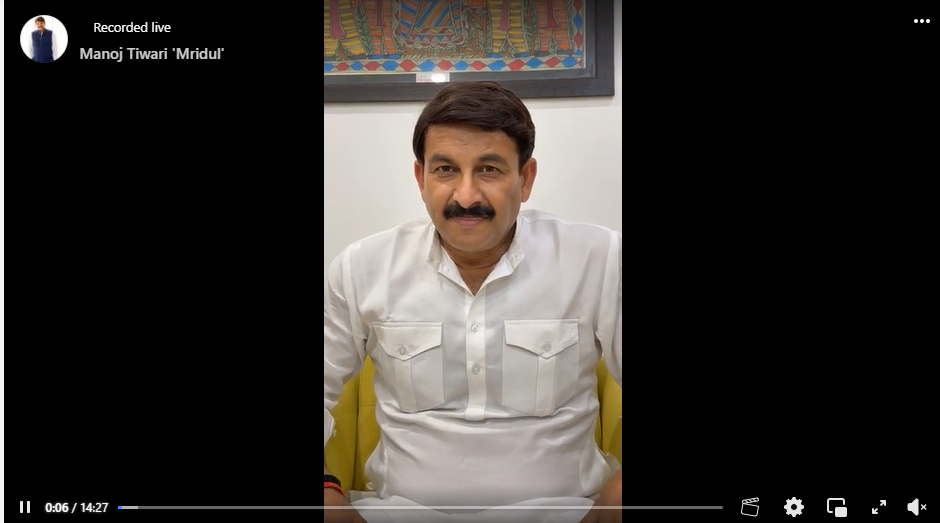

A keyword search on Google did not yield any credible media reports suggesting that Manoj Tiwari had made such a statement. No reliable source was found to support the viral claim. Further research led to a clarification posted on Manoj Tiwari’s official Facebook page. In the video statement, Tiwari categorically denied making any such remark about the rupee and the dollar. He stated that the viral claim being circulated in his name was completely fake.

Manoj Tiwari’s clarification video on Facebook

Conclusion

The viral claim is false. Manoj Tiwari never made any statement suggesting that stopping the use of ₹1 and treating ₹2 as ₹1 would strengthen the rupee against the dollar. He has himself denied the claim and called it fake.

Executive Summary

A social media post about the shooting incident during a dinner event for journalists covering the White House is going viral with the claim that the attacker was a Muslim man who was shot dead by security personnel. The accompanying video shows panic inside a hall and alert security officials responding to the situation. wHowever, research by the CyberPeace Research Wing found that the claim is false and misleading. The video is being shared with incorrect information about the identity and fate of the suspect.

Claim:

An Instagram user shared the video on April 26, 2026, claiming that the attacker who targeted Donald Trump was a “jihadi” named Mohammad Ibrahim and that he was killed after being shot multiple times.

Fact Check:

To verify the claim, relevant keyword searches were conducted online.

A report published by BBC on April 28, 2026, stated that the suspect accused of attempting to assassinate President Donald Trump during the Washington dinner event was identified as Cole Thomas Allen. The report said Allen lived with his parents in Los Angeles and was produced in court on April 28.

According to court documents cited in the report, Allen rushed past a security checkpoint carrying a semi-automatic handgun, a pump-action shotgun, and three knives. Authorities said one Secret Service agent was injured during the incident before Allen was subdued and taken into custody. A separate report published by NBC News on April 26, 2026, also identified the accused as Cole Thomas Allen and included visuals from the incident, showing the suspect after his arrest.

Conclusion:

The claim that the White House dinner party attacker was a Muslim man named Mohammad Ibrahim is false. The accused has been identified as Cole Thomas Allen, and he was arrested after the incident. Claims that he was killed are also incorrect.