#FactCheck: Fake video falsely claims FM Sitharaman endorsed investment scheme

Executive Summary:

A video gone viral on Facebook claims Union Finance Minister Nirmala Sitharaman endorsed the government’s new investment project. The video has been widely shared. However, our research indicates that the video has been AI altered and is being used to spread misinformation.

Claim:

The claim in this video suggests that Finance Minister Nirmala Sitharaman is endorsing an automotive system that promises daily earnings of ₹15,00,000 with an initial investment of ₹21,000.

Fact Check:

To check the genuineness of the claim, we used the keyword search for “Nirmala Sitharaman investment program” but we haven’t found any investment related scheme. We observed that the lip movements appeared unnatural and did not align perfectly with the speech, leading us to suspect that the video may have been AI-manipulated.

When we reverse searched the video which led us to this DD News live-stream of Sitharaman’s press conference after presenting the Union Budget on February 1, 2025. Sitharaman never mentioned any investment or trading platform during the press conference, showing that the viral video was digitally altered. Technical analysis using Hive moderator further found that the viral clip is Manipulated by voice cloning.

Conclusion:

The viral video on social media shows Union Finance Minister Nirmala Sitharaman endorsing the government’s new investment project as completely voice cloned, manipulated and false. This highlights the risk of online manipulation, making it crucial to verify news with credible sources before sharing it. With the growing risk of AI-generated misinformation, promoting media literacy is essential in the fight against false information.

- Claim: Fake video falsely claims FM Nirmala Sitharaman endorsed an investment scheme.

- Claimed On: Social Media

- Fact Check: False and Misleading

Related Blogs

Introduction

AI has penetrated most industries and telecom is no exception. According to a survey by Nvidia, enhancing customer experiences is the biggest AI opportunity for the telecom industry, with 35% of respondents identifying customer experiences as their key AI success story. Further, the study found nearly 90% of telecom companies use AI, with 48% in the piloting phase and 41% actively deploying AI. Most telecom service providers (53%) agree or strongly agree that adopting AI would provide a competitive advantage. AI in telecom is primed to be the next big thing and Google has not ignored this opportunity. It is reported that Google will soon add “AI Replies” to the phone app’s call screening feature.

How Does The ‘AI Call Screener’ Work?

With the busy lives people lead nowadays, Google has created a helpful tool to answer the challenge of responding to calls amidst busy schedules. Google Pixel smartphones are now fitted with a new feature that deploys AI-powered calling tools that can help with call screening, note-making during an important call, filtering and declining spam, and most importantly ending the frustration of being on hold.

In the official Google Phone app, users can respond to a caller through “new AI-powered smart replies”. While “contextual call screen replies” are already part of the app, this new feature allows users to not have to pick up the call themselves.

- With this new feature, Google Assistant will be able to respond to the call with a customised audio response.

- The Google Assistant, responding to the call, will ask the caller’s name and the purpose of the call. If they are calling about an appointment, for instance, Google will show the user suggested responses specific to that call, such as ‘Confirm’ or ‘Cancel appointment’.

Google will build on the call-screening feature by using a “multi-step, multi-turn conversational AI” to suggest replies more appropriate to the nature of the call. Google’s Gemini Nano AI model is set to power this new feature and enable it to handle phone calls and messages even if the phone is locked and respond even when the caller is silent.

Benefits of AI-Powered Call Screening

This AI-powered call screening feature offers multiple benefits:

- The AI feature will enhance user convenience by reducing the disruptions caused by spam calls. This will, in turn, increase productivity.

- It will increase call privacy and security by filtering high-risk calls, thereby protecting users from attempts of fraud and cyber crimes such as phishing.

- The new feature can potentially increase efficiency in business communications by screening for important calls, delegating routine inquiries and optimising customer service.

Key Policy Considerations

Adhering to transparent, ethical, and inclusive policies while anticipating regulatory changes can establish Google as a responsible innovator in AI call management. Some key considerations for AI Call Screener from a policy perspective are:

- The AI screen caller will process and transcribe sensitive voice data, therefore, the data handling policies for such need to be transparent to reassure users of regulatory compliance with various laws.

- AI has been at a crossroads in its ethical use and mitigation of bias. It will require the algorithms to be designed to avoid bias and reflect inclusivity in its understanding of language.

- The data that the screener will be using is further complicated by global and regional regulations such as data privacy regulations like the GDPR, DPDP Act, CCPA etc., for consent to record or transcribe calls while focussing on user rights and regulations.

Conclusion: A Balanced Approach to AI in Telecommunications

Google’s AI Call Screener offers a glimpse into the future of automated call management, reshaping customer service and telemarketing by streamlining interactions and reducing spam. As this technology evolves, businesses may adopt similar tools, balancing customer engagement with fewer unwanted calls. The AI-driven screening will also impact call centres, shifting roles toward complex, human-centred interactions while automation handles routine calls. They could have a potential effect on support and managerial roles. Ultimately, as AI call management grows, responsible design and transparency will be in demand to ensure a seamless, beneficial experience for all users.

References

- https://resources.nvidia.com/en-us-ai-in-telco/state-of-ai-in-telco-2024-report

- https://store.google.com/intl/en/ideas/articles/pixel-call-assist-phone-screen/

- https://www.thehindu.com/sci-tech/technology/google-working-on-ai-replies-for-call-screening-feature/article68844973.ece

- https://indianexpress.com/article/technology/artificial-intelligence/google-ai-replies-call-screening-9659612/

Executive Summary

A video is going viral on social media claiming that a salon has been opened inside a State Bank of India (SBI) ATM in Bihar. The video is also being used by some users to take political jibes at the central and state governments led by the Bharatiya Janata Party (BJP). However, the CyberPeace Research Wing’s research has found that this claim is misleading. The location shown in the viral video was earlier an SBI ATM, which had been shut down around six months ago. After the bank discontinued its operations at the site, the ATM machine and other equipment were removed. However, the external structure of the ATM cabin and the SBI signage were not removed at that time. After the premises were vacated, the property owner rented out the space to a salon operator. Since the SBI board and branding were still visible on the structure, the video created confusion and went viral with misleading claims.

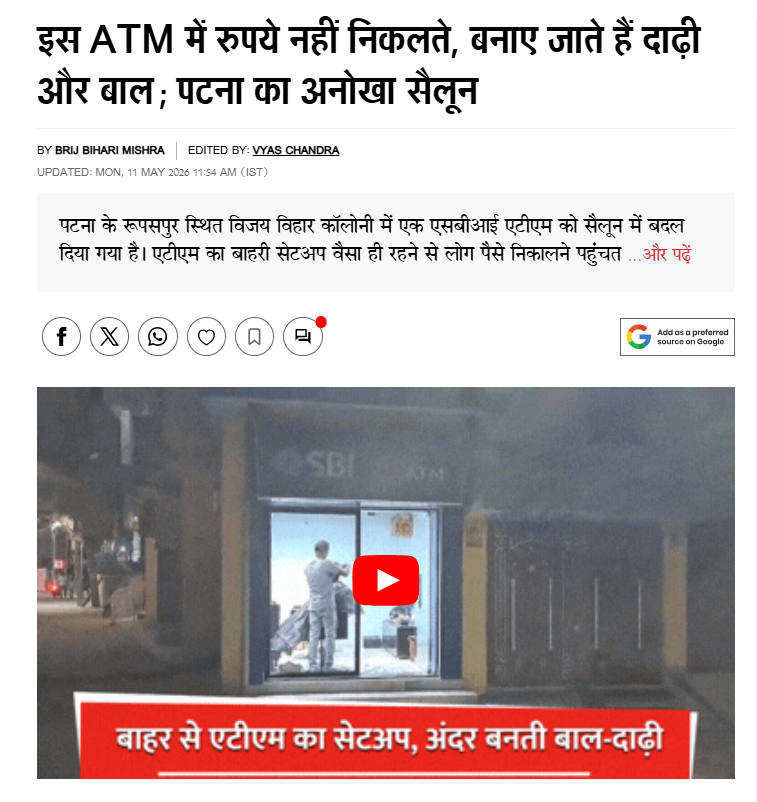

Following the circulation of the video, the bank later removed its signage from the location and also cleared all remaining SBI branding from the structure. Our research also found that the bank had removed the ATM machine and equipment months earlier, but the cabin structure and SBI board were left behind. After that, the space was rented out for commercial use as a salon. In this context, it would be incorrect to claim that a salon was opened inside an active SBI ATM.

Claim

A Facebook user ‘Soumitra Roy’ shared a video on 11 May 2026 claiming:

“Someone has opened a barber shop inside an SBI ATM in Bihar. The BJP’s double-engine government has developed Bihar so much that loan EMIs can now be deducted directly inside ATMs. This is Modi’s masterstroke.”

- https://www.facebook.com/reel/980962511535926

- https://perma.cc/WTY2-WEQQ

Fact Check

To verify the viral claim, a keyword search based on the video was conducted. Several media reports were found, which clarified the full context of the incident. A report uploaded on the YouTube channel ‘Live Cities’ on 12 May 2026 stated that a salon was running at a former ATM location in Danapur, Bihar. The bank had already vacated the premises about six months earlier, but its signage had not been removed. The report also includes an interview with the property owner, who confirmed that the bank had removed its ATM machine and equipment six months ago and later the space was rented out to a salon operator.

The viral video was also found on the Jagran website in a news report dated 11 May 2026. The report states that an SBI ATM previously existed at the location. The bank had removed the ATM machine due to operational reasons but left behind the external structure and signage. Later, the space was rented out to a salon operator, who began running his business from the same setup.

Conclusion

Our research found that the viral post is misleading. It is incorrect to claim that a salon was opened inside an SBI ATM. The truth is that the bank had shut down the ATM at this location around six months ago and removed all machines and equipment. After that, the premises were rented out to a salon operator, which led to confusion due to the presence of old SBI signage.

Executive Summary:

A viral post currently circulating on various social media platforms claims that Reliance Jio is offering a ₹700 Holi gift to its users, accompanied by a link for individuals to claim the offer. This post has gained significant traction, with many users engaging in it in good faith, believing it to be a legitimate promotional offer. However, after careful investigation, it has been confirmed that this post is, in fact, a phishing scam designed to steal personal and financial information from unsuspecting users. This report seeks to examine the facts surrounding the viral claim, confirm its fraudulent nature, and provide recommendations to minimize the risk of falling victim to such scams.

Claim:

Reliance Jio is offering a ₹700 reward as part of a Holi promotional campaign, accessible through a shared link.

Fact Check:

Upon review, it has been verified that this claim is misleading. Reliance Jio has not provided any promo deal for Holi at this time. The Link being forwarded is considered a phishing scam to steal personal and financial user details. There are no reports of this promo offer on Jio’s official website or verified social media accounts. The URL included in the message does not end in the official Jio domain, indicating a fake website. The website requests for the personal information of individuals so that it could be used for unethical cyber crime activities. Additionally, we checked the link with the ScamAdviser website, which flagged it as suspicious and unsafe.

Conclusion:

The viral post claiming that Reliance Jio is offering a ₹700 Holi gift is a phishing scam. There is no legitimate offer from Jio, and the link provided leads to a fraudulent website designed to steal personal and financial information. Users are advised not to click on the link and to report any suspicious content. Always verify promotions through official channels to protect personal data from cybercriminal activities.

- Claim: Users can claim ₹700 by participating in Jio's Holi offer.

- Claimed On: Social Media

- Fact Check: False and Misleading